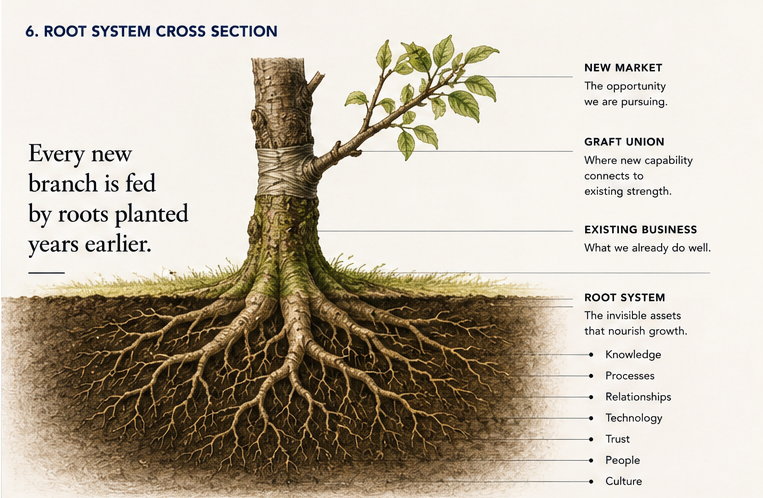

The Adjacency Principle

The opportunities that look biggest in the model are usually the ones whose capability cost has not been priced into the comparison. A twenty-year body of research has been clear on which bets actually carry.

In 2004, Chris Zook and a research team at Bain & Company finished a decade of work on a single question: when public companies grow into new categories, which growth bets actually pay off?

They had data on more than eighteen hundred public companies. The pattern was clear and durable, and slightly inconvenient for how most strategic plans get written. Growth into capabilities adjacent to the existing core, sharing the same customers, operating motion, and go-to-market, succeeded at materially higher rates than growth into unrelated categories. Roughly twice the success rate, with the gap widening past five years.

Edith Penrose articulated the underlying mechanism in 1959. Zook’s contribution was the empirical scaffolding and the language. What is most striking about the finding is how rarely it shows up in actual growth decisions.

Most strategic plans evaluate growth options on opportunity size. These are the right questions; they are not the only ones. The variable consistently under-weighted is the cost of building the capabilities the new category requires.

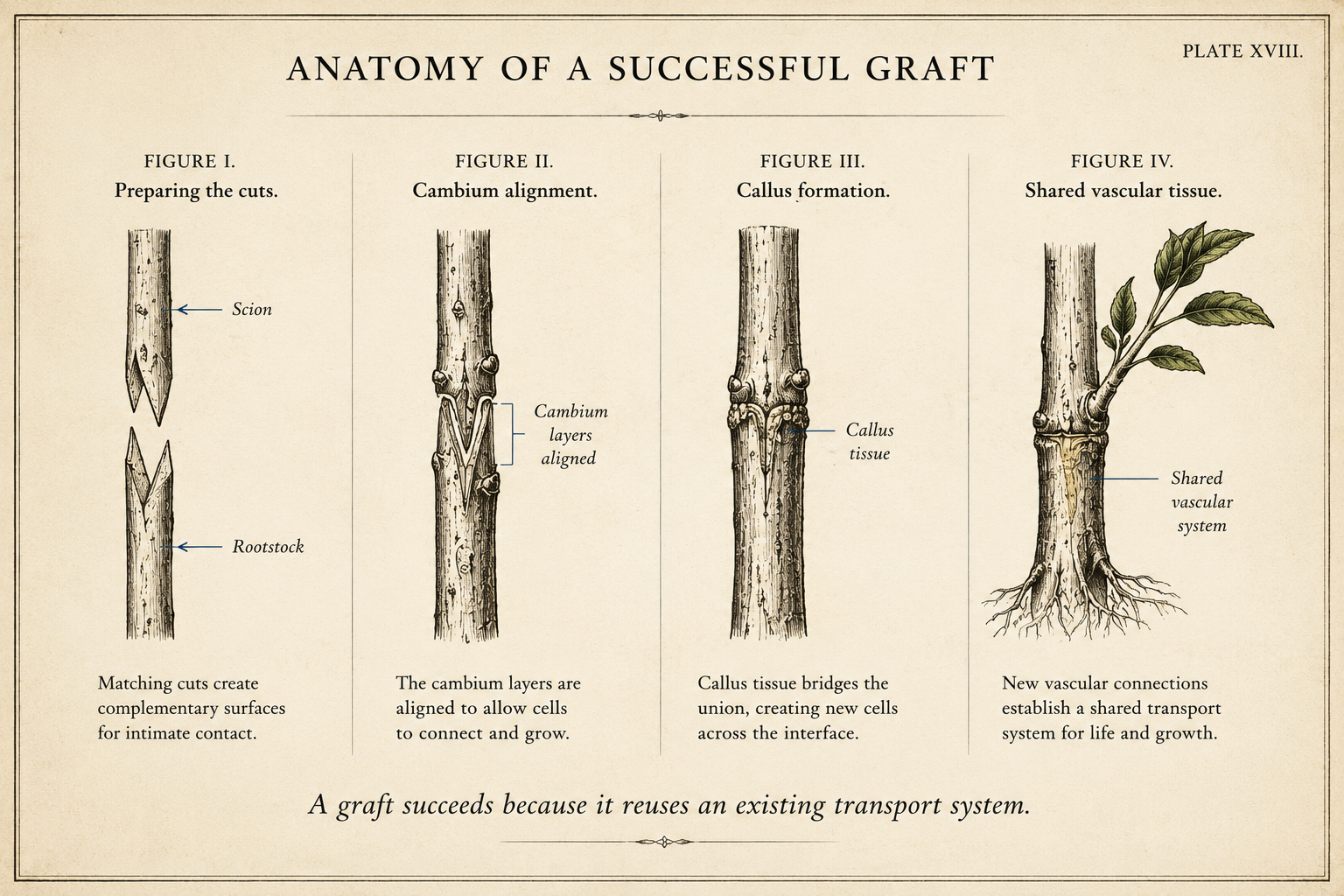

The unfamiliar category looks bigger because the existing capability set is, at best, partially relevant. The opportunity is actually two opportunities. The market entry, plus the capability build. Priced as one.

The adjacent category looks smaller because most of the capability build is invisible: customer relationships and operating motion already exist, and the infrastructure transfers. The smaller revenue figure reaches the budget cycle. The adjacency loses on the strength of an apples-to-oranges comparison the strategy committee did not notice it was making.

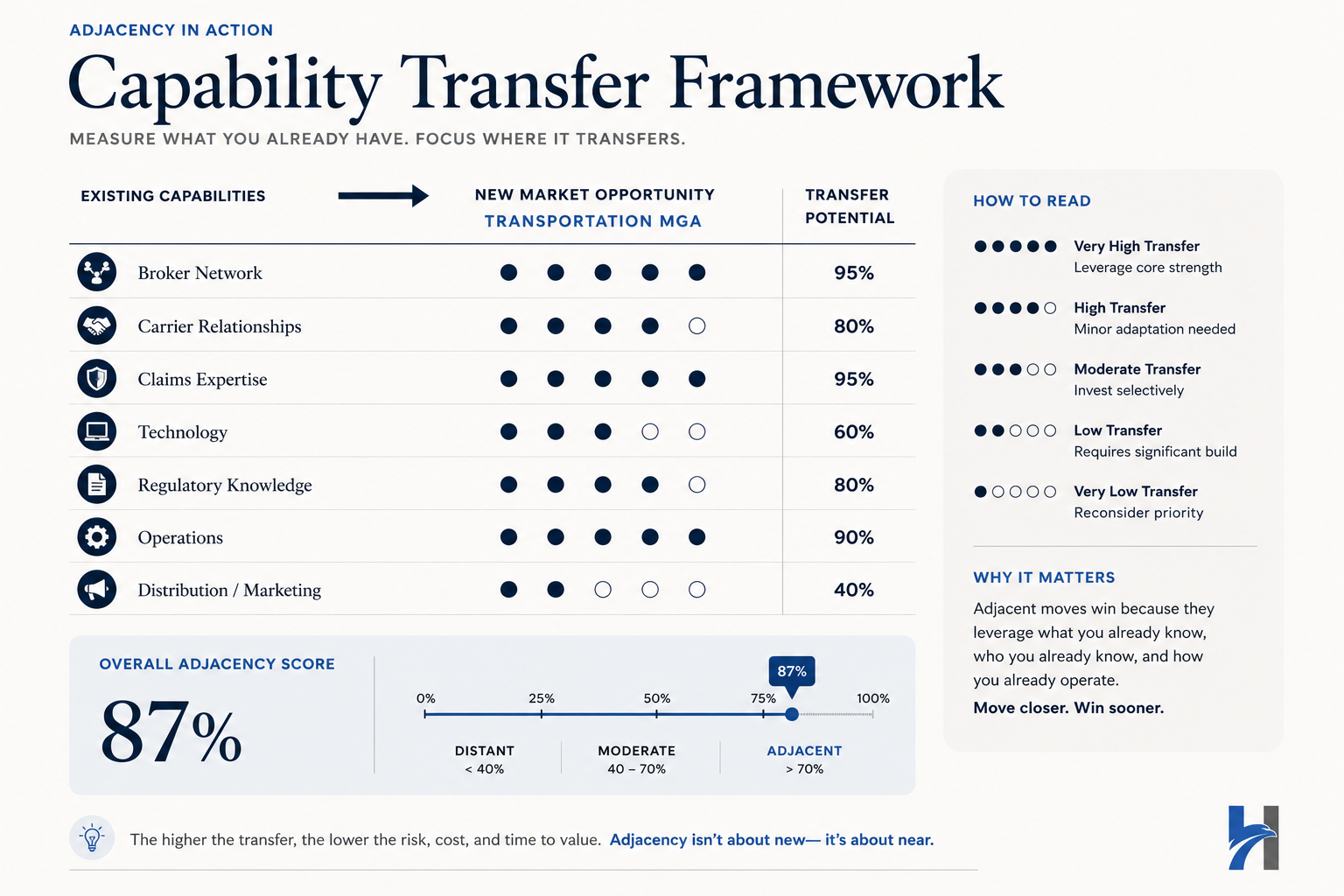

A scenario from specialty insurance makes the math visible.

A specialty carrier with a strong professional liability book is offered two expansion options. Option A: a management liability program targeting the same broker partners and client size band, under the same underwriting frame. Year-three GWP uplift: a modest 30 percent on the existing book. Option B: a transportation program with 2.4 times the projected GWP. It had no shared distribution and no shared underwriting frame, and the infrastructure did not transfer.

Leadership selects transportation on the strength of the projection. Three years later, transportation GWP is 60 percent of projection. The carrier’s professional liability core has lost two underwriters to the transportation build, and the broker community has noted the carrier’s reduced focus on its anchor line. The management liability program, which the carrier did not pursue, has launched at a competitor.

The capability cost was the difference. It was real. It was not in the comparison.

Leaps do work, sometimes. The Bain finding is statistical, not categorical. Adjacency is not a substitute for category selection. What the research is clear on, across twenty years, is that the adjacency premium widens with time. At the eighteen-month mark, adjacency and leap can look similar. At the five-year mark, the patterns diverge sharply. Adjacency is not the safer bet because it is more conservative. It is the stronger bet because the capabilities it requires were already mostly built.

The same logic, slightly shifted, governs partner selection.

When carriers expand operational capacity, the partner whose operating style is structurally close to the carrier’s, with a comparable operating rhythm and a shared vocabulary around appetite and exception, produces accumulating returns because the integration cost is low and the operational seams disappear.

A partner whose style is materially different produces returns that look identical at signature and behave very differently in execution. The same adjacency principle that governs which line of business to enter governs which partner to enter it with.

The carriers that have grown most successfully across two underwriting cycles share a common practice. They evaluate growth options on two variables, opportunity size and capability distance, and they treat both with equal rigor. The leap is occasionally available and occasionally appropriate; they take it deliberately, with the capability cost priced in.

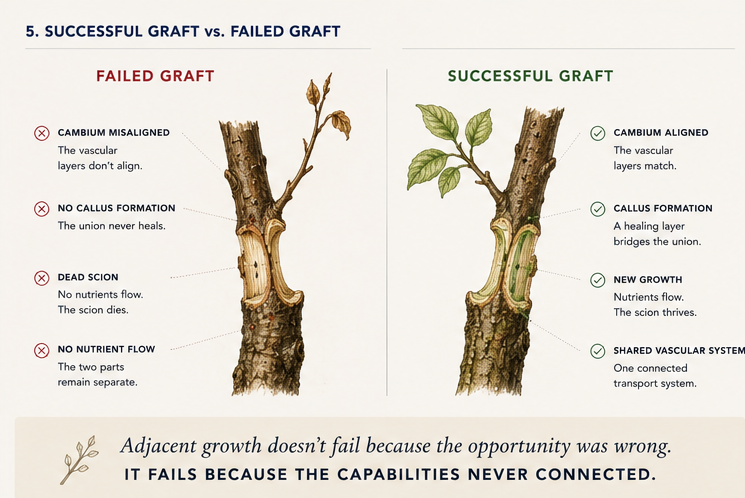

The growth that compounds is the growth closest to what you already do. The discipline is recognizing it before the opportunity model has hidden the comparison.